In onze vorige blog over diversificatie, bespraken we het doel van diversificatie, de voordelen ervan en hoe het je portefeuille beïnvloedt. Nu gaan we in op de wiskunde achter portefeuille diversificatie en hoe moderne portefeuilletheorie werkt.

Moderne portefeuilletheorie

De moderne portefeuilletheorie (MPT) is een beleggingsleer die beleggers in staat stelt een portefeuille samen te stellen die het verwachte rendement maximaliseert bij een gegeven risiconiveau. MPT werd in 1952 geïntroduceerd door Harry Markowitz in zijn paper 'Portfolio Selection'. Hij toonde wiskundig aan dat beleggers, door activa te combineren die niet perfect gecorreleerd zijn, het totale portefeuillerisico konden verlagen. Voorheen hielden beleggingsstrategieën geen rekening met correlatie tussen investeringen.

Het werk van Markowitz leidde tot optimalisatietechnieken die beleggers helpen portefeuilles samen te stellen op basis van hun risicoprofiel. Bijvoorbeeld, voor deze institutionele beleggers:

Pensioenfonds A

Een looptijd van 5 jaar

200.000 deelnemers

3,5 miljard euro aan beheerd vermogen

Een dekkingsgraad van 138%

Pensioenfonds B

Een looptijd van 28 jaar

5.400.000 deelnemers

260 miljard euro aan beheerd vermogen

Een dekkingsgraad van 105%

Volgens MPT:

Moet Pensioenfonds A zich richten op risicobeperking, kortetermijndiversificatie en stabiele rendementen.

Moet Pensioenfonds B zich richten op langetermijninvesteringen met spreiding, waarbij hogere risico's worden genomen voor een hoger potentieel rendement.

Het kernidee van Markowitz is dat risico een eigenschap is van de hele portefeuille, niet van individuele activa. De bijdrage van een enkele investering aan het totale risico hangt af van zowel het gewicht in de portefeuille als de interactie met andere activa.

’Mean-Variance’ analyse

Markowitz introduceerde de ‘Mean-Variance’ analyse, waarbij het gemiddelde (μ) staat voor het verwachte rendement van de portefeuille, en de variantie (σ²) of standaarddeviatie (σ) het risico (volatiliteit) van de rendementen weergeeft. Beleggers worden verondersteld risicomijdend te zijn, en streven ernaar om het rendement te maximaliseren bij een bepaald risico of het risico te minimaliseren bij een gewenst rendement.

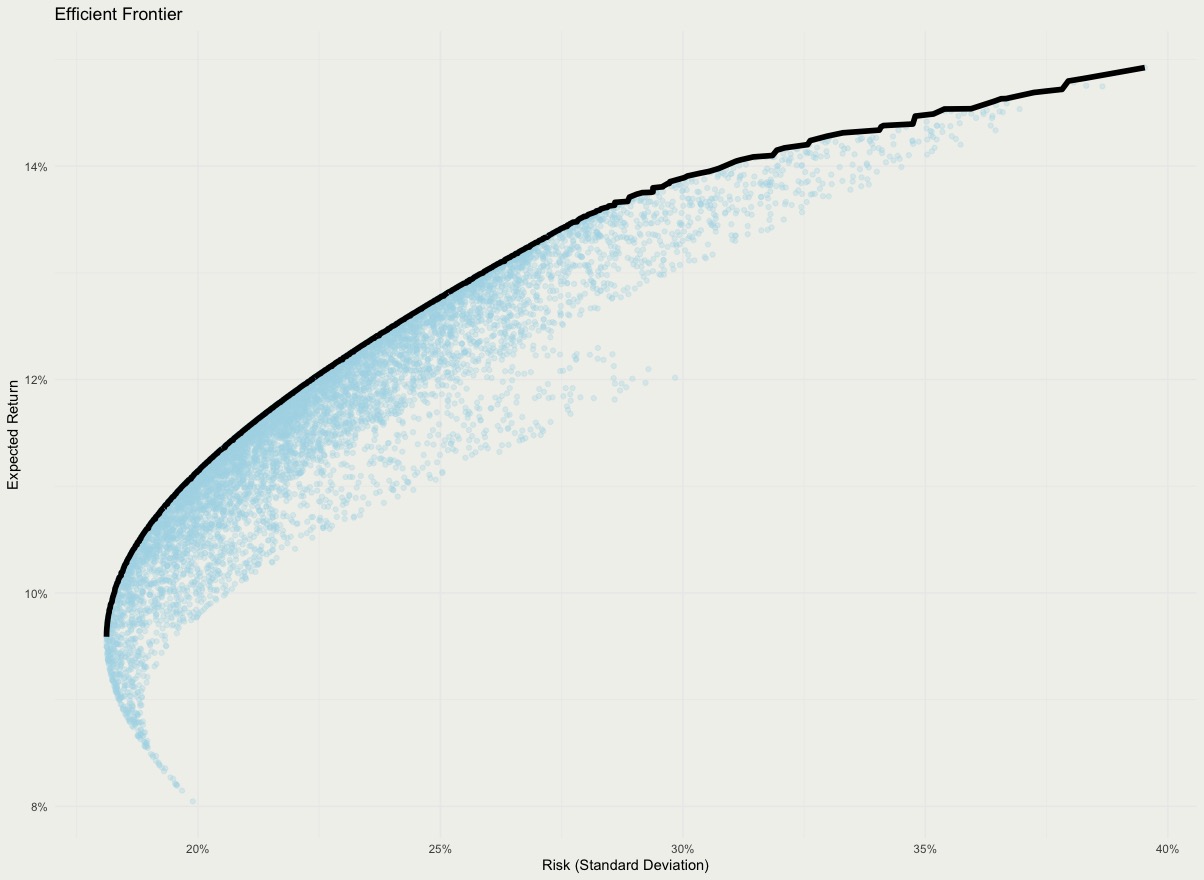

Efficiënte grens

Een van de meest invloedrijke bijdragen van MPT is de efficiënte grens — een reeks optimale portefeuilles die het hoogste verwachte rendement bieden bij een bepaald risiconiveau. Elke portefeuille op de efficiënte grens wordt als efficiënt beschouwd, wat betekent dat er geen andere portefeuille is met:

Een hoger verwacht rendement bij hetzelfde risiconiveau, of

Een lager risico bij hetzelfde verwachte rendement.

Portefeuilles die zich niet op de efficiënte grens bevinden, worden als suboptimaal beschouwd omdat ze te veel risico nemen voor het rendement of te weinig rendement opleveren voor het genomen risico.

Wiskundig begrip van diversificatie

Markowitz loste het probleem op met behulp van kwadratische optimalisatietechnieken. Het doel van de belegger is:

Minimaliseer de variantie van de portefeuille:

minwTΣw

waarbij:

wTis de getransponeerde gewichten van de activa in het portfolio

Σis de covariantiematrix van de activa in het portfolio

w is het gewicht van de activa in het portfolio

Het minimaliseren van de portfoliovariantie is een kernobjectief bij het samenstellen van een portfolio, vooral voor risicomijdende beleggers. Het betekent in wezen het selecteren van een mix van activa op een manier dat het totale risico—of de variabiliteit in rendementen—zo laag mogelijk is, gegeven de correlaties tussen de activa. Deze formule laat zien dat de variantie niet alleen afhankelijk is van de individuele varianties van de activa, maar ook van de covariantie (of correlatie) tussen hen.

Onder de voorwaarde van een doelrendement μ,

wTμ=μp

i=1∑nwi=1

Deze twee beperkingen betekenen dat het portfolio een beoogd verwacht rendement moet behalen en dat de gewichten van alle activa in het portfolio samen 1 moeten zijn (d.w.z. het portfolio is volledig geïnvesteerd)

Covarianties meenemen: Portefeuillerisico hangt niet alleen af van de individuele varianties van activa, maar ook van hun covarianties (hoe ze samen bewegen). Diversificatie wordt bereikt door bezittingen te selecteren met een lage of negatieve correlatie.

Als een portefeuille uit twee activa bestaat, wordt het risico (de variantie) van de portefeuille berekend met:

σp2=wA2σA2+wB2σB2+2wAwBσAσBρAB

waarbij:

wA,wB= gewichten van activa A en B in de portefeuille

σA,σB= standaarddeviaties van de rendementen van activa A en B

ρAB= correlatiecoëfficiënt tussen activa A en B

Impact van correlatie (ρ)

Als ρ=1, wordt de variantie van de portefeuille niet verminderd (perfect positieve correlatie).

Als ρ=0, bestaat de variantie van de portefeuille alleen uit de eerste twee termen (niet-gecorreleerde activa).

Als ρ<0, wordt het gecombineerde risico verminderd, wat leidt tot grotere voordelen van diversificatie.

Correlatie is dus een sleutelfactor bij het bepalen van portefeuillerisico.

Rendement van een portefeuille berekenen

Het rendement van een portefeuille is simpelweg het gewogen gemiddelde van de rendementen van de individuele activa:

Rp=i=1∑nwiRi

Voor een portefeuille met twee activa:

Rp=wARA+wBRB

waarbij:

wA,wB= de gewichten van activa A en B in de portefeuille

RA,RB= de rendementen van activa A en B in de portefeuille

Diversificatie Voorbeeldberekening

Beschouw een eenvoudig portfolio bestaande uit twee activa: een Veilige Activa met een consistent rendement van 5%, en een Risicovolle Activa met rendementen van 40% in een goed scenario en -20% in een slecht scenario.

In een slecht scenario zou investeren alleen in de Risicovolle Activa -20% opleveren. Een gediversifieerd portfolio met 50% toewijzing aan elk activa levert echter op: 0,5 x 5% + 0,5 x (-20%) = -7,5%, wat het neerwaartse risico aanzienlijk vermindert.

In een goed scenario, terwijl de Risicovolle Activa 40% kan opleveren, levert het gediversifieerde portfolio: 0,5 x 5% + 0,5 x 40% = 22,5%, waarmee een groot deel van het opwaartse potentieel wordt benut.

Diversificatie vermindert dus extreme verliezen terwijl het nog steeds aanzienlijke winsten mogelijk maakt, waardoor het risico en de beloning effectiever in balans worden gebracht dan bij investeren in een enkel activa.

Tot slot over diversificatie

Dit is een vereenvoudigde uitleg van diversificatie met een portefeuille van twee activa. In de echte wereld zijn portefeuilles veel complexer, maar het basisprincipe blijft hetzelfde: diversificatie vermindert risico door activa op te nemen die niet perfect gecorreleerd zijn.

Diversificatie is echter geen garantie tegen verliezen. Beleggers moeten ook rekening houden met:

Het bijhouden van meerdere portefeuilles kan uitdagend zijn. De Figy vereenvoudigt portefeuillebeheer door je bezittingen inzichtelijk te maken op basis van type, sector en valuta. Zo krijg je een helder beeld van je diversificatiestrategie en kun je rendement beter afwegen tegen risico.

In het volgende deel van deze serie gaan we dieper in op de meest toegepaste strategieën voor diversificatie. In het laatste deel van de serie onderzoeken we of diversificatie daadwerkelijk mogelijk is in een onderling verbonden wereld.

Belangrijke opmerking: Dit artikel vormt geen financieel advies. Raadpleeg een professional voor financieel advies.

Glossarium

Moderne portefeuilletheorie (MPT)

Een beleggingsleer die beleggers helpt een geoptimaliseerde portefeuille samen te stellen waarbij risico en rendement in balans zijn.

Diversificatie

Een risicobeheersingsstrategie waarbij beleggingen worden verspreid over verschillende bezittingen om blootstelling aan één enkele bezitting te beperken.

Harry Markowitz

De econoom die in 1952 de moderne portefeuilletheorie introduceerde.

’Mean-Variance’ analyse

Een wiskundige methode om portefeuilles te evalueren op basis van verwachte rendementen en risico (variantie).

Verwacht rendement

Het verwachte rendement op een investering, gebaseerd op historische gegevens of waarschijnlijkheidsinschattingen.

Variantie

Een maatstaf voor de spreiding binnen een dataset, die het risico of de volatiliteit van een actief of portefeuille vertegenwoordigt.

Standaarddeviatie

De wortel van de variantie, gebruikt om de variatie in rendementen van een bezitting te kwantificeren.

Efficiënte grens

Een reeks optimale portefeuilles die het hoogste verwachte rendement bieden bij een gegeven risiconiveau.

Kwadratische optimalisatie

Een wiskundige techniek om portefeuillerisico te minimaliseren bij het behalen van een gewenst rendement.

Portefeuillevariantie

De totale risicomaat van een portefeuille, berekend op basis van individuele varianties van activa en hun onderlinge correlaties.

Covariantie

Een statistische maatstaf voor hoe twee activarendementen samen bewegen, wat invloed heeft op het totale portefeuillerisico.

Correlatie

Een waarde tussen -1 en 1 die aangeeft hoe activa zich ten opzichte van elkaar bewegen.

Zwarte-zwaan gebeurtenis

Een onvoorspelbare, zeldzame gebeurtenis met grote impact op financiële markten, vaak relevant bij risicobeoordeling.